Powered By

Powered By

Your Dream Retirement Awaits

Your Retirement Awaits

CALL 877-377-9802

Planning for retirement is one of the most important decisions you will make in life. That's why we believe finding the right financial information is instrumental in helping you achieve your financial goals.

CUSTOM JAVASCRIPT / HTML

Planning for retirement is one of the most important decisions you will make in life. That's why we believe finding the right financial information is instrumental in helping you achieve your financial goals.

CUSTOM JAVASCRIPT / HTML

A Powerful Approach To

Retirement Planning

At Annuity National, we take a different and powerful approach to retirement planning. Our team of experienced professionals will ask you a few simple questions and within a few minutes, we will match you with a local Annuity National representative in your area. We're able to cover almost every city and town in the U.S.

At Annuity National, we take a different and powerful approach to retirement planning. Our team of experienced professionals will ask you a few simple questions and within a few minutes, we will match you with a local Annuity National representative in your area. We're able to cover almost every city and town in the U.S.

Are you over 50?

Get up to 33% more in retirement income.*

Increased income is possible by following a specific strategy suited to your financial goals. Call now for our free book from a leading national firm in maximizing retirement income.

We make it easy

Make smart and informed financial decisions.

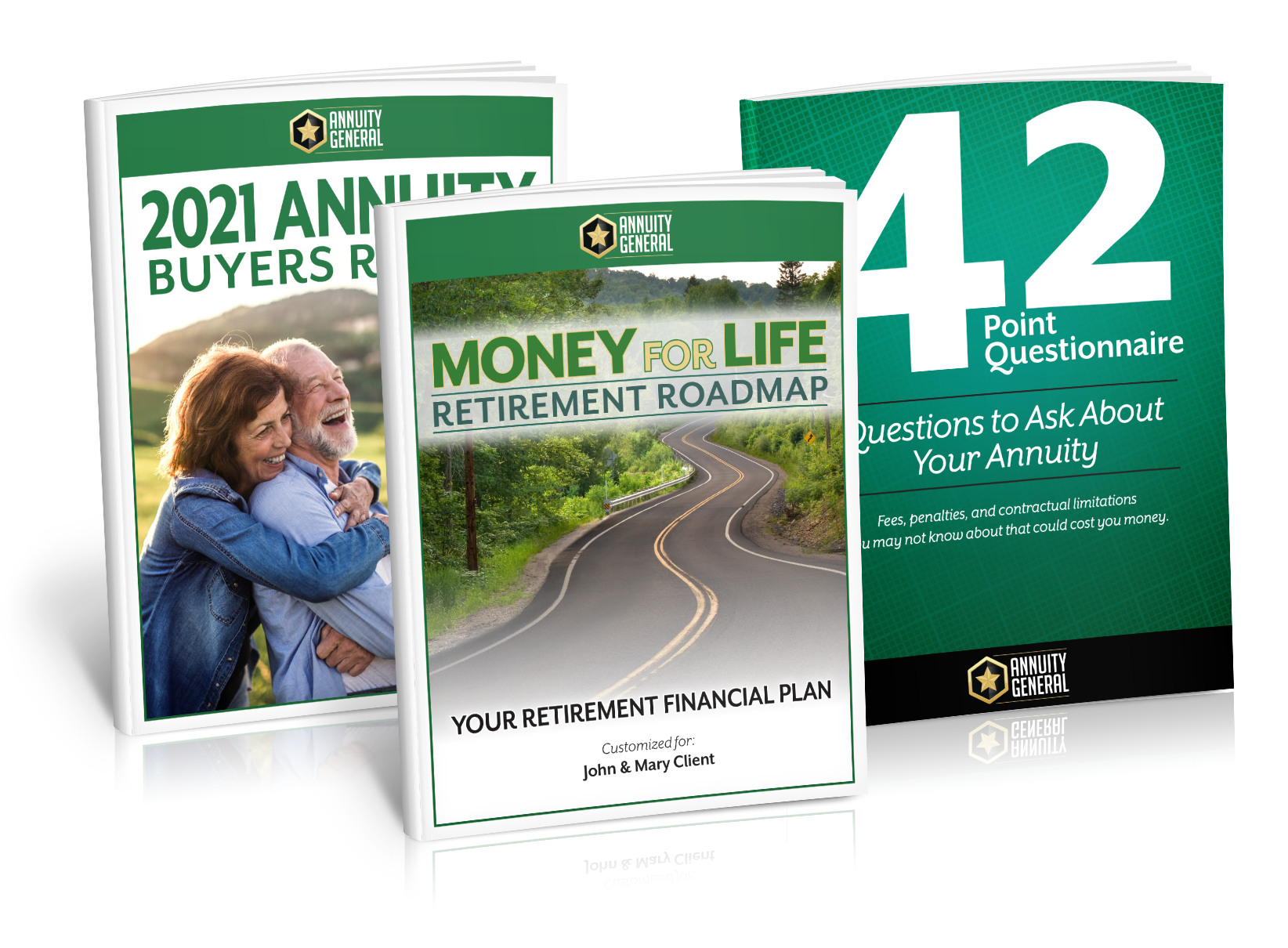

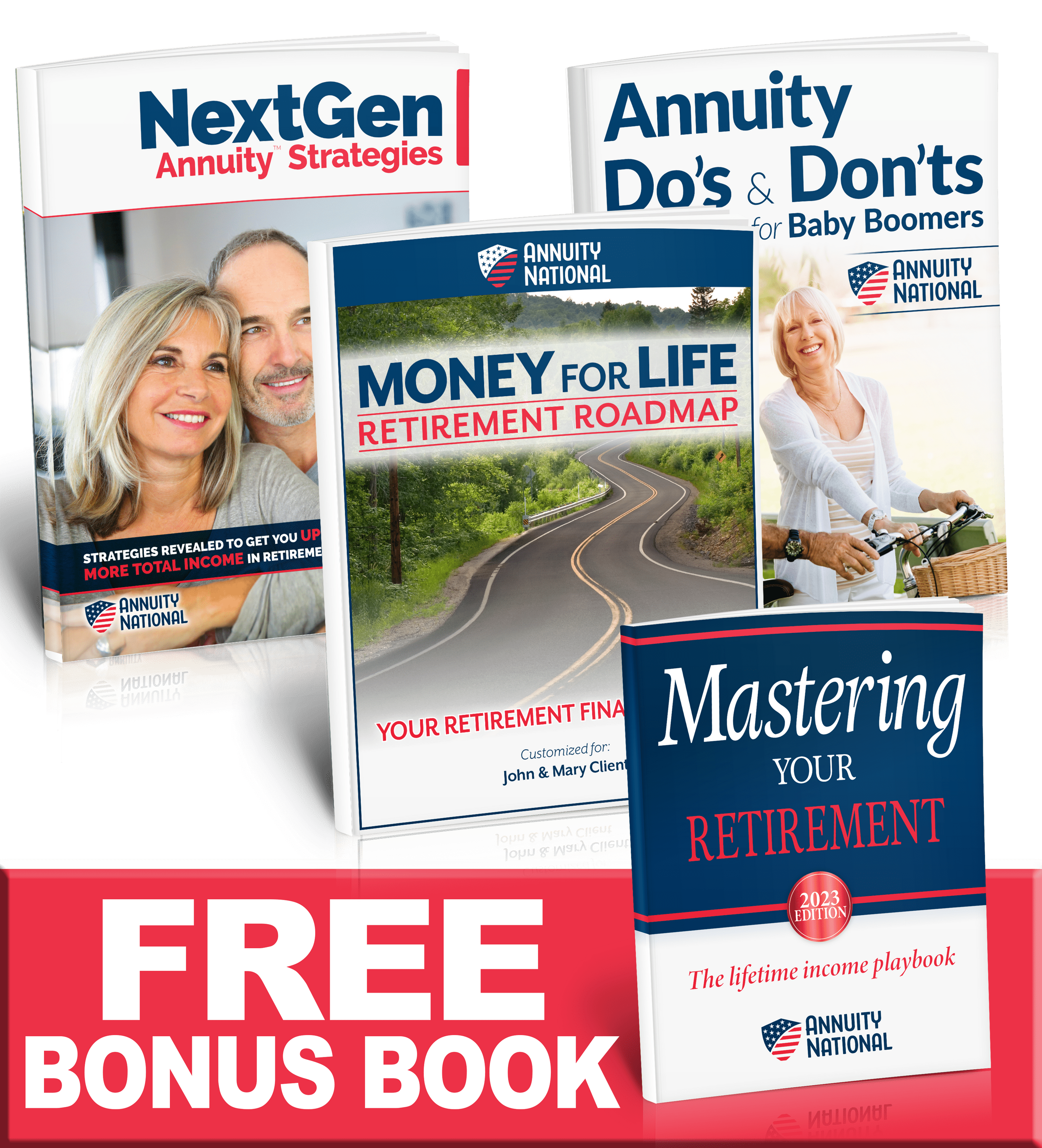

Education is the key to a successful retirement, which is why we've created several resources to help you learn more about annuities and determine if they're the right fit for you . Our materials are FREE and our guides can help give you the confidence you need to make the right financial decisions in retirement.

CUSTOM JAVASCRIPT / HTML

Annuities Explained

With all the different types of annuities out there, we know it can be difficult to understand how they work. One of the most important things you need to know is that annuities are not investment vehicles. Annuities are long-term insurance contracts that can provide a guaranteed stream of income during retirement that you cannot outlive. **

We firmly believe that education is the key to a successful retirement, which is why we've created several resources to help you learn more about annuities and determine if they're the right fit for you. Our materials are FREE and our guides can help give you the confidence you need to make good financial decisions.

Our approach is different. We are committed to developing comprehensive educational materials and tools aimed to make one of the most important decisions in life easy and enjoyable. Don't wait. Call now for your free resources.

CUSTOM JAVASCRIPT / HTML

CALL 877-377-9802

This page is not intended for residents of Idaho.

Please note that the examples herein are not company nor product specific. They are concepts shown to give you general information of the benefits and limitations of the products and strategies and are not designed to be a recommendation to buy any specific financial product or service. Products change and such product concepts may not be suitable for your needs or available in your state.

Annuity guarantees rely on the financial strength and claims-paying ability of the issuing insurance company and are not guaranteed by any bank or the FDIC.

Annuity National is not associated with or endorsed by the Social Security Administration, the IRS or any government agency.

Caller will be contacted by Allied Elite Financial, LLC, DBA Annuity National and may be put in touch with an insurance licensed producer regarding retirement income planning using fixed insurance products. Allied Elite Financial, LLC is insurance licensed in all 50 states (AR17677332/CAOK62245/TX2034282) and all producers have the appropriate licenses for the products they offer. This is an advertisement.

*Based on a 2023 analysis of Annuity National recommended strategies compared to average competitor results. Individual results will vary based on your single premium amount, age at application, age at rider exercise, and the specific annuity contract and rider combination you select. Contact Annuity National for details.

**A fixed annuity income rider must be selected at application and provides guaranteed income payments for life if contract and rider conditions are met. Income payments are considered withdrawals from the annuity and will reduce the annuity's contract value. Riders involve an additional fee that is deducted annually from the contract value. Contact your insurance producer for details and consult the applicable product and rider disclosures for a more complete description of features, benefits, and restrictions. All applications are subject to insurer approval.

Product features, riders and availability may vary by state. Guarantees are based on the claims-paying ability of the issuing company. Nassau does not provide individual tax, financial or investment advice or act as a fiduciary in the sale or service of insurance contracts. Please consult your personal tax or financial advisor for assistance. Nassau has a financial interest in the sale of its products.

Annuities are long-term insurance products particularly suitable for retirement assets. Annuities are not meant to be used to meet short-term financial goals. Annuities held within qualified plans do not provide any additional tax benefit. Early withdrawals may be subject to surrender charges, recovery of non-vested premium bonus, market value adjustment and applicable pro-rated rider and strategy fees. Withdrawals are subject to ordinary income tax, and if taken prior to age 59½, a 10% IRS penalty may also apply.

Non-Security Status Disclosure - These contracts have not been approved or disapproved by the Securities and Exchange Commission. The contracts are not registered under the Securities Act of 1933 and are offered and sold in reliance on an exemption therein.

Nassau Personal Income Annuity (19FIA, ICC19EIAN, 19ISN, 19GLWB2, ICC19GLWB2.1, ICC19GLWB2.2) single premium deferred fixed indexed annuities are issued by Nassau Life and Annuity Company (Hartford, CT). In California, Nassau Life and Annuity Company does business as "Nassau Life and Annuity Insurance Company." Nassau Life and Annuity Company is not authorized to do business in ME and NY, but that is subject to change. Nassau Life and Annuity Company is a subsidiary of Nassau Financial Group. Insurance Products: Not FDIC/NCUAA Insured, No Bank/Credit Union Guarantee. BPD41517

Allied Elite Financial, LLC, DBA Annuity National

Annuity National| Copyright ©2023 | All Rights Reserved |